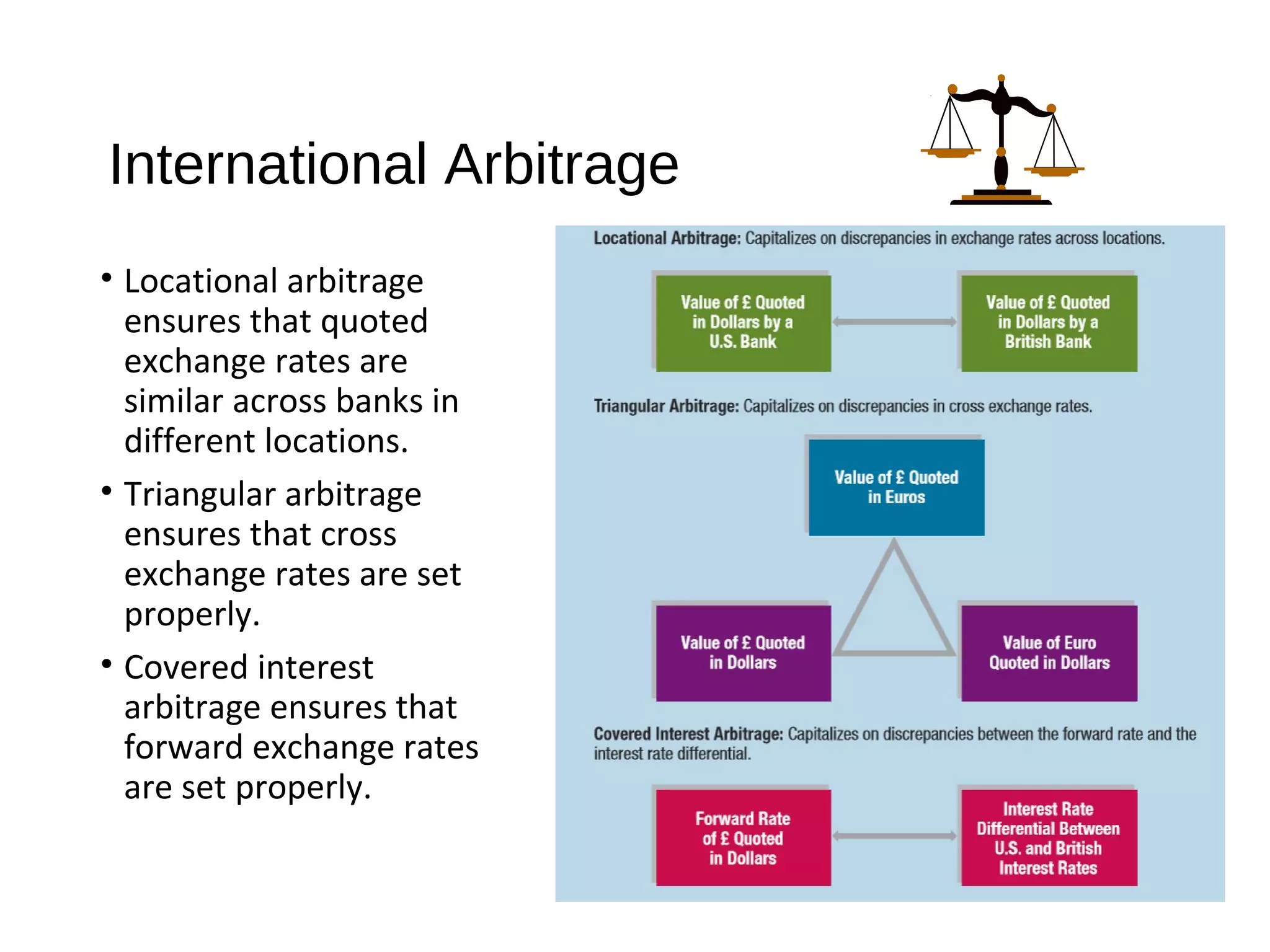

The recent $4 billion capital raise by Eldridge Industries alumni—operating under the banner of Hunter Point Capital—represents more than a successful fundraising cycle; it is a calculated bet on the fragmentation of the private equity GP-stakes market. As traditional buyout shops face liquidity constraints and a frozen IPO market, a secondary layer of institutionalization is forming. This $4 billion injection targets a specific structural bottleneck: the inability of mid-sized alternative asset managers to monetize their own enterprise value while simultaneously funding the GP commits required for larger, more frequent fund vintages.

The Mechanism of General Partner Stakes

The private capital ecosystem functions on a tiered incentive structure. At the base lies the Limited Partner (LP) capital, which fuels the investments. Above this sits the General Partner (GP), which manages the assets. The GP-stakes model involves an outside firm buying a minority equity interest in the management company of the private equity firm itself. This is not an investment in a specific fund, but an investment in the "factory" that produces the funds. For an alternative look, see: this related article.

The current market environment has created a liquidity trap for these "factories." Several variables drive this necessity for external capital:

- GP Commit Scaling: As fund sizes grow from $500 million to $2 billion, the required GP commitment (typically 1-2% of the fund) increases from $5 million to $40 million. Management fees, often used to fund these commits, are frequently recycled back into the business, leaving senior partners "asset rich but cash poor."

- Succession Friction: Founders of mid-market firms require a liquidity event to transition ownership to the next generation of leadership without crippling the firm's balance sheet.

- Platform Expansion: To remain competitive, firms must diversify from pure buyout strategies into private credit, infrastructure, or real estate. This requires immediate balance sheet capital that annual management fees cannot provide.

The Three Pillars of Value Capture

The strategy deployed by the Milken-network alumni identifies three specific inefficiencies in how private capital firms are currently valued and scaled. Related analysis regarding this has been published by Reuters Business.

1. Revenue Stream Diversification

Institutional investors are no longer satisfied with the volatility of carried interest (performance fees). They prioritize the stability of Management Fee Related Earnings (FRE). By acquiring stakes in firms with high FRE margins, Hunter Point is essentially buying a high-yield annuity protected by long-term lock-up periods. This shifts the risk profile from "can this manager pick winners?" to "can this manager keep raising capital?"

2. Operational Industrialization

Mid-market firms often operate with the administrative infrastructure of a boutique while managing billions in assets. The "value-add" component of the $4 billion raise involves a "platform services" model. By centralizing functions such as capital formation, ESG reporting, and back-office technology across their portfolio of GPs, GP-stakes firms create a margin expansion that the individual firms could not achieve in isolation. This is an exercise in industrializing the middle office.

3. Capital Scarcity Arbitrage

We are currently in a "denominator effect" environment where LPs are over-allocated to private equity because their public equity holdings have fluctuated or remained stagnant. This has created a bottleneck for new fundraises. Firms with a GP-stakes partner gain a "seal of approval" and access to a broader network of global institutional capital, effectively bypassing the bottleneck that is currently stifling their competitors.

The Cost Function of Capital Recycling

To understand the scale of this $4 billion raise, one must analyze the capital recycling velocity within a private equity firm. When a firm sells a portfolio company, the profits are distributed. However, if the firm wishes to grow, it must reinvest its share of those profits into the next fund.

If the internal rate of return (IRR) on a firm’s own management company exceeds the IRR of its underlying investments, the firm is incentivized to sell a stake in itself to fund growth. This creates a feedback loop. The $4 billion pool acts as a catalyst in this loop, providing the "bridge equity" necessary for mid-market firms to jump into the upper-middle market.

The Risks of Oversaturation and Valuation Drift

While the thesis for GP stakes is structurally sound, it is not without significant execution risk. The primary threat is the compression of yields due to an influx of competing capital.

- Entry Multiple Inflation: As more firms like Hunter Point, Blue Owl (Dyal), and Goldman Sachs (Petershill) compete for a limited pool of high-quality mid-market GPs, the entry multiples for these management companies are pushed higher. If a firm buys in at 15x FRE and the market cools, the path to a profitable exit via IPO or secondary sale narrows significantly.

- Alignment Erosion: The core appeal of private equity is the alignment of interests between the GP and the LP. If a GP sells 20% of its management company and 20% of its carry to an outside firm, the "skin in the game" for the individual deal partners is diluted. This can lead to a culture shift where the focus moves from generating alpha (outperformance) to maximizing AUM (Assets Under Management) to satisfy the new equity holders.

- Concentration of Influence: The "Milken alumni" network effect suggests a consolidation of power within a small circle of operators. While this provides a powerful sourcing engine, it also creates systemic risk. If one major GP-stakes player faces a liquidity crisis, it could trigger a forced sell-off across dozens of underlying private equity firms simultaneously.

The Shift from Stock Picking to System Building

The move by this $4 billion fund signals a definitive transition in the industry. Private equity is moving away from its roots as a collection of savvy individual investors and toward a model of permanent capital vehicles. The target firms are no longer just "investment managers"; they are being rebuilt as "financial institutions."

This institutionalization requires a different set of KPIs. Performance is no longer measured solely by a 3.0x Multiple on Invested Capital (MOIC). Instead, the metrics that matter for this $4 billion deployment are:

- AUM Retention Rate: The percentage of LPs who re-up into subsequent fund vintages.

- FRE Margin Expansion: The ability to lower the cost of managing each dollar of capital through scale and automation.

- GP-Stake Yield: The quarterly cash distributions from the management company back to the stake-holder.

Competitive Dynamics in the Mid-Market

The mid-market (firms managing between $1 billion and $10 billion) is the current battlefield for this capital. These firms are large enough to have proven track records but small enough to benefit meaningfully from institutional scaling. Large-cap firms (those over $50 billion AUM) are generally already public or have internal liquidity mechanisms.

The $4 billion raise specifically targets this "missing middle." By providing the capital for these firms to professionalize their investor relations, upgrade their data analytics, and expand geographically, the GP-stakes firm creates a competitive moat around its portfolio GPs. A mid-market firm with an institutional partner will inherently out-compete a "solo" firm for talent and LP mindshare.

Logical Framework of the LP Perspective

For the Limited Partners who contributed to this $4 billion fund, the logic is one of "Inception-style" diversification. By investing in a GP-stakes fund, an LP is getting exposure to:

- The management fees of 15-20 different private equity firms.

- The carried interest from hundreds of underlying portfolio companies.

- The enterprise value growth of the management companies themselves.

This represents a superior risk-adjusted return compared to investing in a single private equity fund. It provides a "look-through" into the broader health of the private capital markets while maintaining a cushion of steady management fee income.

Strategic Allocation of the $4 Billion

The deployment of this capital will likely follow a structured sequencing:

- Tier 1: Liquidity Provision (40%): Purchasing stakes from retiring founders to stabilize the cap table of target GPs.

- Tier 2: Growth Equity (30%): Funding the launch of new product lines (e.g., a buyout firm launching a credit arm) to increase the total addressable market (TAM) of the GP.

- Tier 3: Working Capital & Tech (20%): Upgrading the operational stack of the GPs to improve reporting transparency and LP satisfaction.

- Tier 4: Opportunistic Co-investment (10%): Providing "top-up" capital for the GPs' most promising deals, allowing the stake-holder to capture more of the upside on high-conviction trades.

The emergence of this $4 billion fund is a symptom of a maturing asset class. When the management of the money becomes as profitable as the money itself, the industry has reached a stage of structural permanence. The success of this fund will depend on whether its managers can act as "architects" of firms rather than just "collectors" of assets.

The immediate tactical move for mid-market GPs is to audit their internal enterprise value. Firms must prepare for the "institutionalization audit"—ensuring their management fee structures, succession plans, and operational workflows are capable of withstanding the scrutiny of a GP-stakes acquirer. Those who fail to professionalize will find themselves starved of the GP-commit capital necessary to survive the next decade of private capital consolidation.